As the mother of electronic products, the PCB industry has also experienced a slight decline in market size due to poor terminal market conditions. Fortunately, starting from 2024, the PCB market size will recover and grow year by year. Among them, IC carrier boards, as a key substrate for advanced packaging of integrated circuits, will lead the growth rate in the next five years.

According to research firm Prismark, the global PCB output value in 2023 is estimated to be $78.367 billion, a decrease of 4.13% from $81.741 billion in 2022. However, it will resume annual growth starting from 2024, with an average compound annual growth rate of 3.8% from 2023 to 2027.

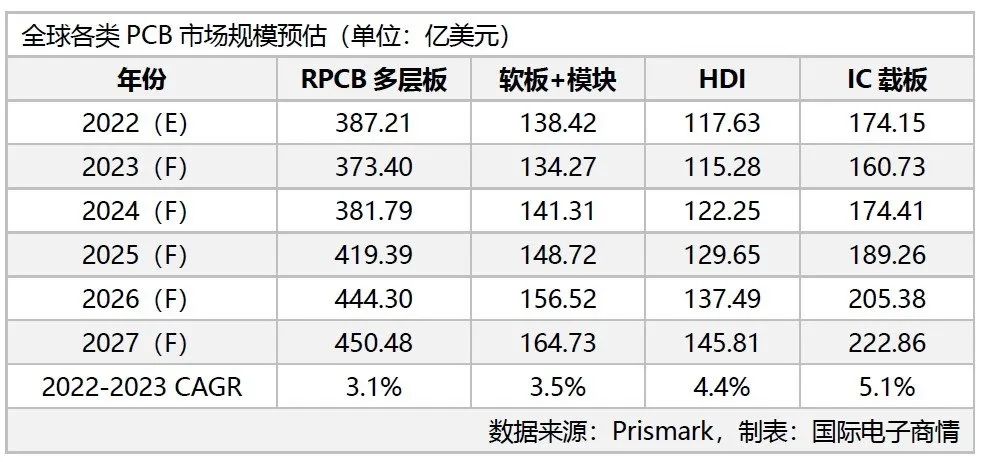

Despite the recession in 2023, the market generally expects that the market will stabilize and demand will gradually recover from the second half of 2023 or 2024 onwards. Prismark's estimated data also shows that the entire industry will resume positive growth from 2024 onwards. The average compound annual growth rates of the four major product lines from 2023 to 2027 are 3.1%, 3.5%, 4.4%, and 5.1%, respectively.

It is not difficult to find that as a key substrate for advanced packaging of integrated circuits, IC carrier boards have potential for growth.

IC carrier board is developed based on the relevant technology of PCB board, used to establish signal connection between IC and PCB. In addition, it can also protect circuits, fix circuits, and dissipate waste heat. It has the characteristics of high density, high precision, miniaturization, and thinness. In the field of high-order packaging, IC carrier boards have replaced traditional lead frames and become an indispensable part of chip packaging, not only providing support, heat dissipation, and protection for chips; Simultaneously providing electronic connections between chips and PCB motherboards, playing a bridging role.

According to analysis, the IC carrier board industry has experienced significant decline this year due to poor demand despite rapid growth in the past few years. With the expected recovery of market demand in 2024, IC carrier boards may usher in new opportunities.

The market pattern of IC carrier plates was first led by Japanese manufacturers, and then the production capacity was transferred to Taiwan, China and South Korea along with the semiconductor industry chain. In recent years, under the impact of manufacturers in South Korea and Taiwan, China, Japanese enterprises have withdrawn from the middle and low-end market and turned to high-end packaging substrates such as FC BGA and FC CSP. At present, the top three IC carrier companies are Xinxing Electronics, Ibiden and Samsung Electromechanical in Taiwan, China, accounting for 15%, 11% and 10% of the market shares respectively.